Snapchat has published its latest performance update, which shows good potential, in terms of ongoing usage growth, but also, some significant concerns on the revenue side.

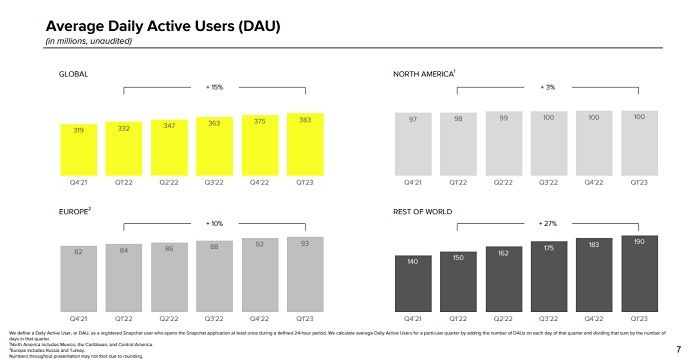

First off, on active users – Snap added 8 million more total daily actives in Q1, taking it to 383 million daily users.

Though as you can see, its growth is essentially flat in the US, its most lucrative market, and EU.

Snap does, however, continue to gain momentum in the ‘Rest of World’ category, with Indian users, in particular, warming to the app. As connectivity and accessibility increases in the region, along with other developing markets, Snap’s gradually expanding its footprint, which bodes well for its future prospects.

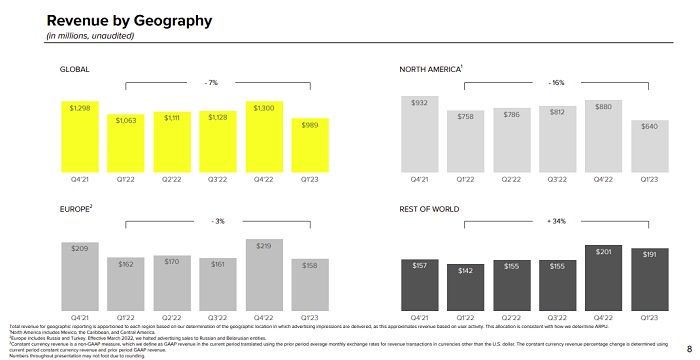

But right now, in terms of revenue, not so great.

As you can see in these charts, Snap brought in $989 million in total for the quarter, a noted decline.

As explained by Snap:

“Q1 revenue was particularly challenged, as we implemented significant changes to our ad platform that were disruptive to demand. While the macroeconomic environment has shown signs of stabilization, it continues to be a headwind to growth. Our brand-oriented business was down 12% year-over-year and our direct-response (DR) business was down 9% year-over-year.”

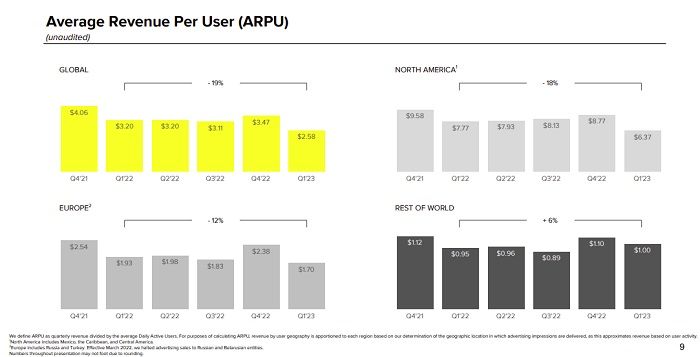

Snap says that it is seeing some improvement in ad performance, as a result of systematic improvements, but right now, its charts don’t look great.

Like, look at this:

That’s not good, especially when you also factor in the major variance between its income in the US and other markets.

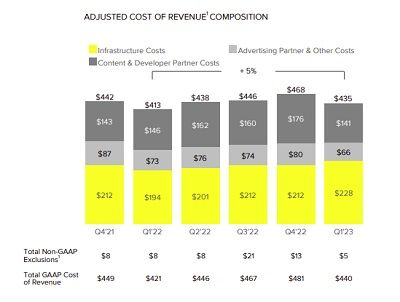

Making matters worse, Snap’s system costs are also rising:

Snap has managed to reduce some of these impacts by cutting staff, but its infrastructure expenses continue to rise, as it continues to develop its AR tools and processes, with a view to maintaining a lead in the space.

This is a key element that Snap will need to manage, as it looks to rationalize its business.

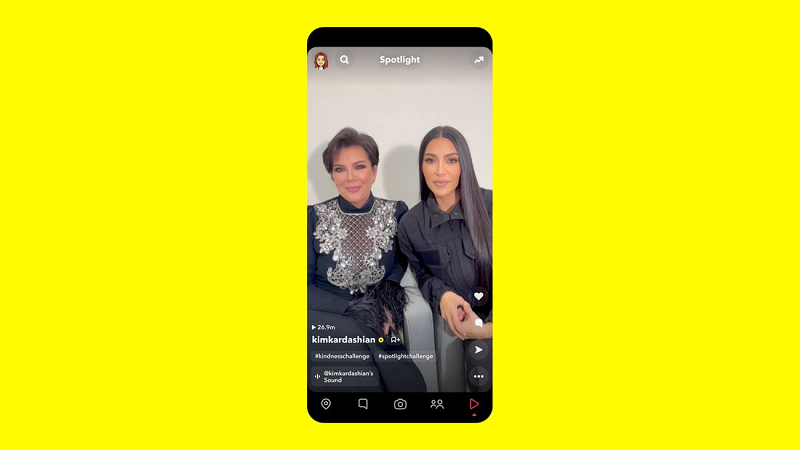

In terms of usage trends, Snapchat says that Spotlight, its TikTok-like feed of short-form video content, has seen significant growth, with more than 350 million monthly active users now engaging with Spotlight content, up 46% year-over-year.

The growth of short-form video is part of broader shift away from ‘social’ elements, and towards entertainment, which is seeing users spend more time in apps, but interact less, and also tap through on posts at lower rates. From a marketing perspective, this is a key trend of note, as it points to the importance of creating content that focuses on entertainment, not on driving referral traffic, as such – which is obviously not as directly beneficial, but may help to increase brand awareness.

Another rising revenue consideration is Snapchat+, its subscription add-on element, which is now up to 3 million paying subscribers.

That’s funneling more money into Snap’s coffers, but as with all platforms, it remains a minor element, with only 0.40% of Snap’s total active user base (750 million MAU) signing on, resulting in an extra $36 million in direct payments.

To be clear, that extra cash is likely worth the effort of maintaining Snapchat+ as an offering. But it pales in comparison to the $989 in total revenue that Snap generated in the quarter.

Until these numbers get somewhere close to each other, subscription elements like this will remain a minor, supplemental consideration – i.e. you’re not going to have to pay to play on all social apps any time soon.

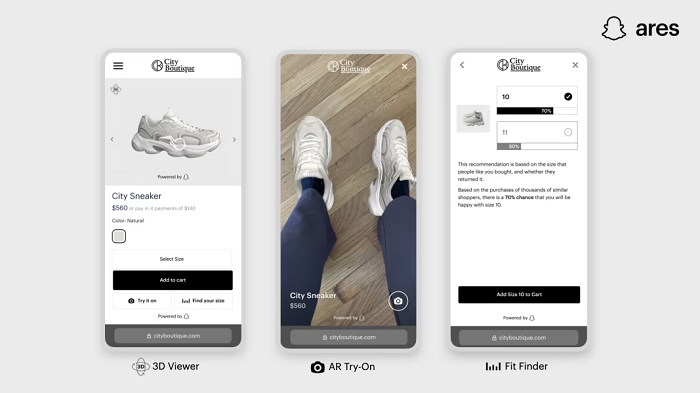

Snap’s also looking to broaden its revenue horizons with its new ARES third-party AR development platform, which enables businesses to use Snap’s AR tools in their own apps and processes.

Snap only launched ARES late last month, so it’s not relevant in a revenue sense as yet, but the idea is that this will better enable Snap to remain a leader in the AR space – and if AR glasses do become a thing, Snap will be well-placed to hold its ground in the sector, even if it isn’t able to release its own AR Spectacles to compete with Apple and Meta direct.

Though Snap is still developing its AR glasses, and could still release them before others. Snap’s fairly secretive about its development, and as noted, it has also dealt with staff cuts, but it is still working on the next stage of its Spectacles offering.

Overall, it’s not a great report card from Snap, but it’s pretty much in line with expectations, given the broader economic impacts that Snap has warned investors about previously. The market is unlikely to be more understanding as a result, but the numbers do fit into the projections that Snap’s been sharing – though it’s not a great time for Snap right now.